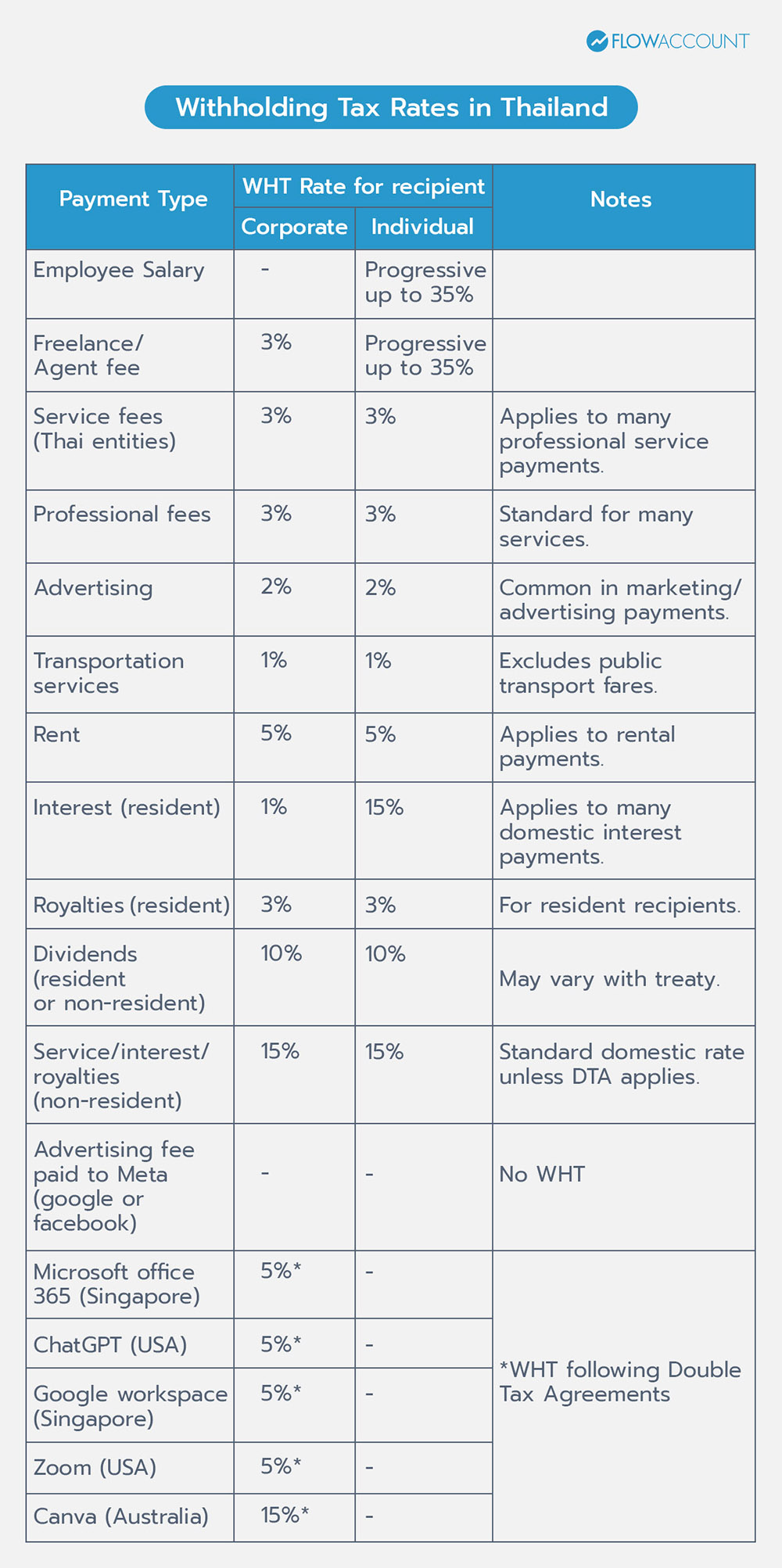

Withholding Tax Rates in Thailand

Withholding tax rates in Thailand vary depending on the type of payment and the recipient’s tax status.

Domestic withholding tax rates generally depend on the nature of the expense, while payments made to non-residents are subject to standard rates unless reduced under a Double Tax Agreement (DTA).

For most service fees, royalties, and interest payments made to foreign companies, the withholding tax rate is typically 15%.

Dividend payments to non-residents are generally subject to a 10% withholding tax rate. Below is a practical summary of the most common withholding tax rates in Thailand.

How to Calculate Withholding Tax in Thailand

Withholding tax is calculated on the net amount before VAT. WHT is not applied to VAT amounts — only the base payment amount is used.

Formula:

WHT = Payment × Tax Rate

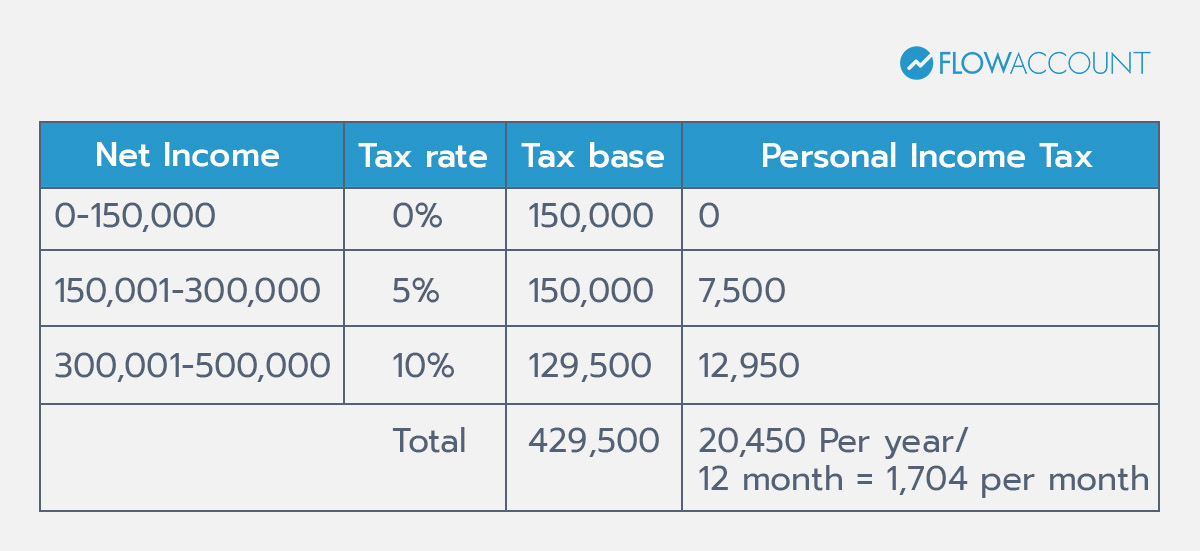

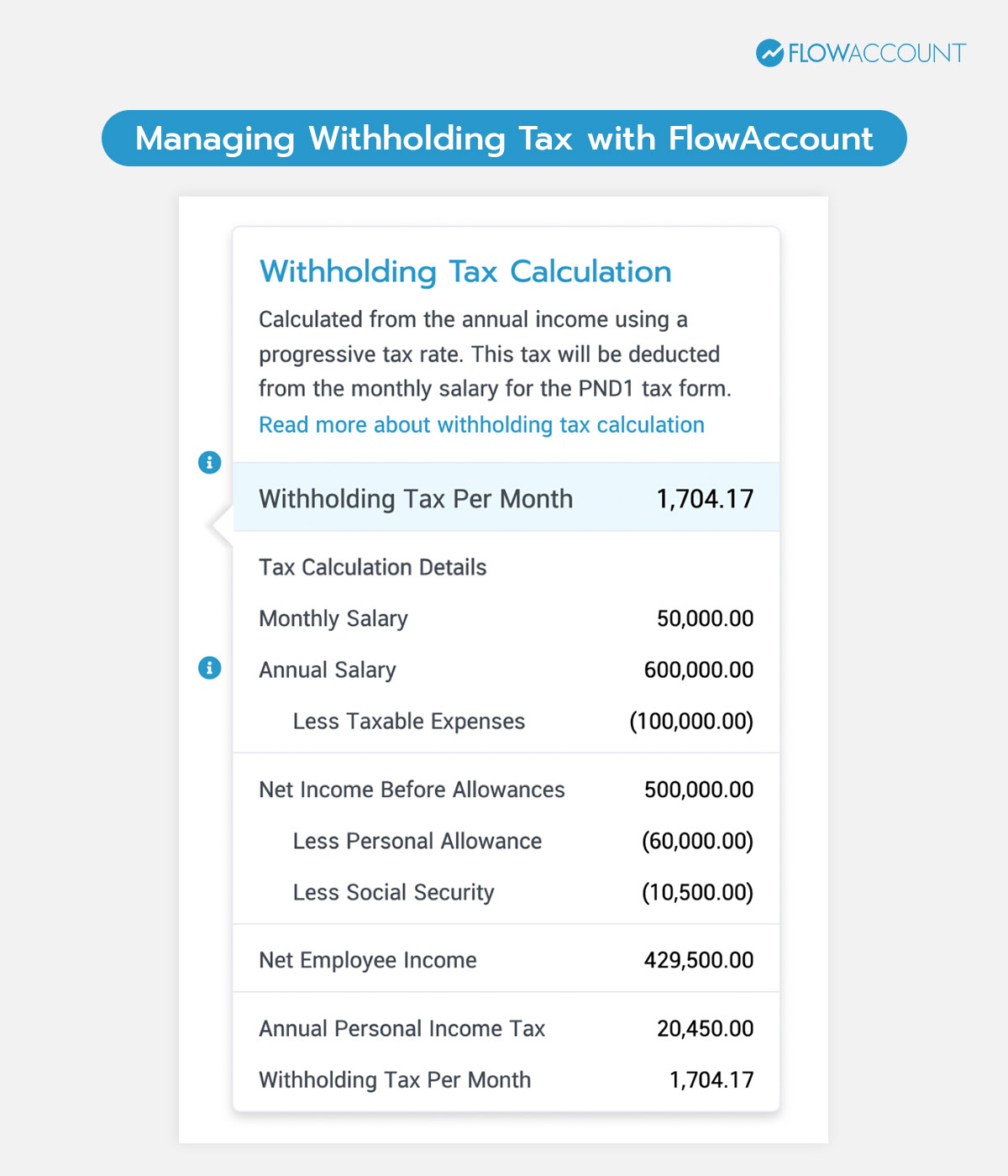

Example 1: Employee Salary (Progressive WHT)

In Thailand, employers withhold tax on employee salaries using progressive personal income tax rates.

Suppose an employee earns THB 50,000 per month. The calculation below applies after considering the standard deduction.

Example 2: Service Fee with VAT

Suppose your company pays a service invoice:

- Net service fee: THB 100,000

- VAT (7%): THB 7,000

- Total invoice: THB 107,000

With a 3% WHT rate (e.g., for professional fees):

- WHT = THB 100,000 × 3% = THB 3,000

- Amount to supplier = THB 107,000 − THB 3,000 = THB 104,000

The THB 3,000 withheld is remitted to the Thai Revenue Department, and the supplier receives a withholding tax certificate to claim the tax credit.

Late submission penalties

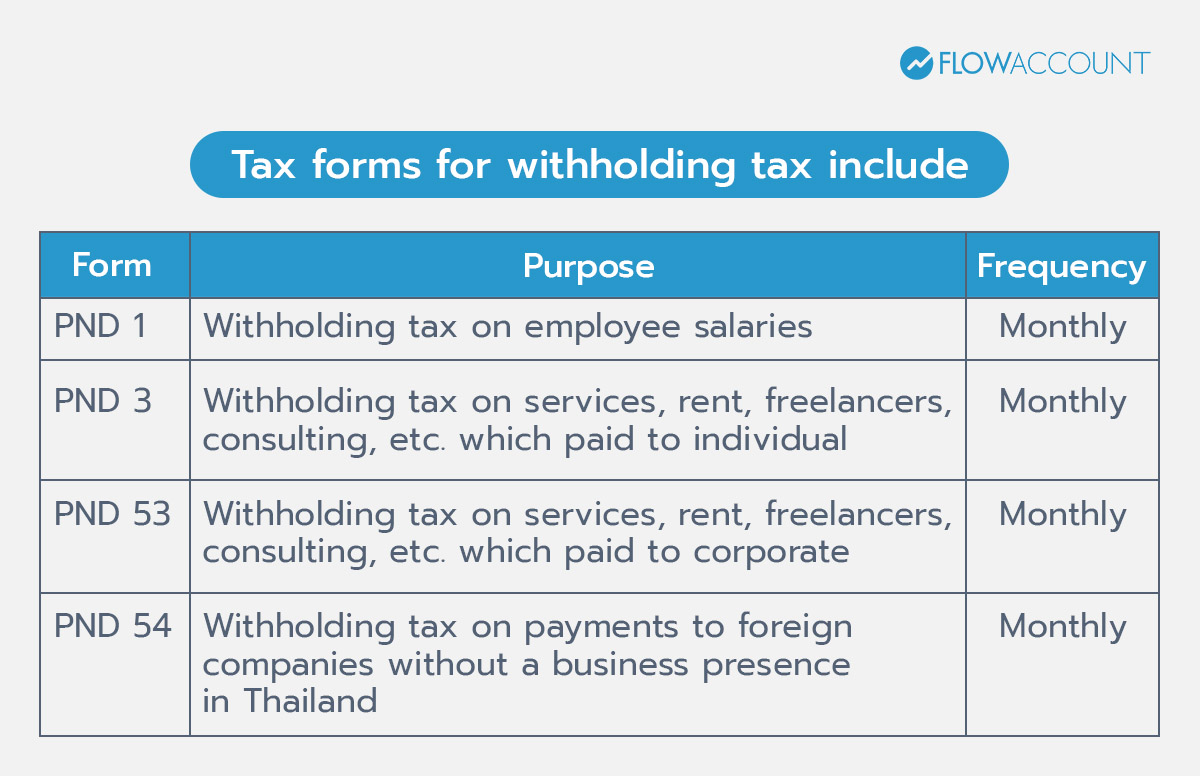

When tax is withheld, the payer must prepare and submit a withholding tax return to the Revenue Department. The filing deadline depends on the submission method: the 7th of the following month for paper filing and the 15th for e-filing. The tax form used also depends on the type of income and the type of payee.

Tax forms for withholding tax include:

If withholding tax returns are not filed on time, penalties and surcharges may apply under Thai tax law.

If the return is late:

- The fine is THB 100 if filed within 7 days after the due date.

- The fine increases to THB 200 if filed more than 7 days late.

- In addition, a 1.5% monthly surcharge is charged on any unpaid tax. Even part of a month is counted as a full month.

To avoid unnecessary costs, businesses should ensure that withholding tax is filed and paid on time each month.

Managing Withholding Tax with FlowAccount

Managing withholding tax requires accuracy, consistency, and proper documentation, which can be time-consuming, especially for those new to Thailand’s tax system.

FlowAccount helps simplify the process by:

- Recording expenses

- Calculating withholding tax automatically

- Generating withholding tax certificates with accuracy, which can be printed, shared via link, or sent directly by email to the payee

FlowAccount also prepares files ready for online withholding tax filing, reducing manual work and errors. By simplifying the entire process, FlowAccount allows business owners and accountants to work more efficiently.

As a result, monthly withholding tax can be managed and submitted quickly, smoothly, and with confidence.

(FAQs) Withholding Tax in Thailand

1. What types of income are subject to withholding tax in Thailand?

Answer: Income such as service fees, rent, royalties, interest, and dividends are commonly subject to WHT. The applicable rate depends on the type of income and recipient.

2. Are foreigners exempt from withholding tax?

Answer: Foreign recipients are generally subject to withholding tax.

However, rates may be reduced or exempt under a Double Tax Agreement if conditions are met.

3. How often do companies need to file withholding tax returns?

Answer: Withholding tax returns must generally be filed monthly. The filing deadline depends on whether paper filing (7th of the following month) or e-filing (15th of the following month) is used.

4. What happens if withholding tax is underpaid or late?

Answer: Penalties and surcharges apply, and the payer remains responsible for the unpaid tax.

5. Are there ways to reduce withholding tax legally?

Answer: Yes. Using Double Tax Agreements and proper documentation can reduce withholding tax legally.

6. How much is withholding tax in Thailand?

Answer: Domestic withholding tax rates commonly range from 1% to 5%.

For foreign payments, rates are typically 10% or 15%, unless reduced by treaty.

7. Which services do 1% and 2% withholding tax rates apply to?

Answer: The 1% rate often applies to transport or certain service payments.

The 2% rate is commonly used for advertising services in Thailand.

8. How to avoid 15% withholding tax?

Answer: The 15% rate cannot be avoided unlawfully.

However, it may be reduced by applying a Double Tax Agreement with proper documents.

9. Who needs to pay withholding tax?

Answer: In simple terms, the tax is paid by the person who receives the income. However, under Thailand’s withholding tax system, the payer deducts the tax from the payment before paying the recipient and remits it to the tax authorities

About Author

Certified Public Accountant (CPA) Thailand with experience as an external auditor for listed companies who aspires to make accounting easy and accessible for everyone.

Apply to be a writer for FlowAccount here.