This article introduces a document that many people are familiar with but might not fully understand how to utilize. We’ll explore what a purchase order (PO) actually is, when it should be used, and how it should be routed within the procurement cycle to ensure effective control.

What is a Purchase Order (PO)?

A purchase order (PO) is an extension of a purchase requisition (PR). The purchase requisition is an internal company document used to inform the management or leaders that the company needs to purchase a certain thing such as raw materials or office equipment. The purchase requisition must get approved before forwarding it to the purchasing department.

A purchase order (PO), on the other hand, is an agreement to buy goods or services, specifying details such as the quantity and price. It is typically used by the purchasing department to confirm orders with an external party.

Purchase orders should involve comparing offers from at least three suppliers to ensure the best quality and price. It must also be approved by an authorized person at each specific price range before sending it to the supplier to place the order.

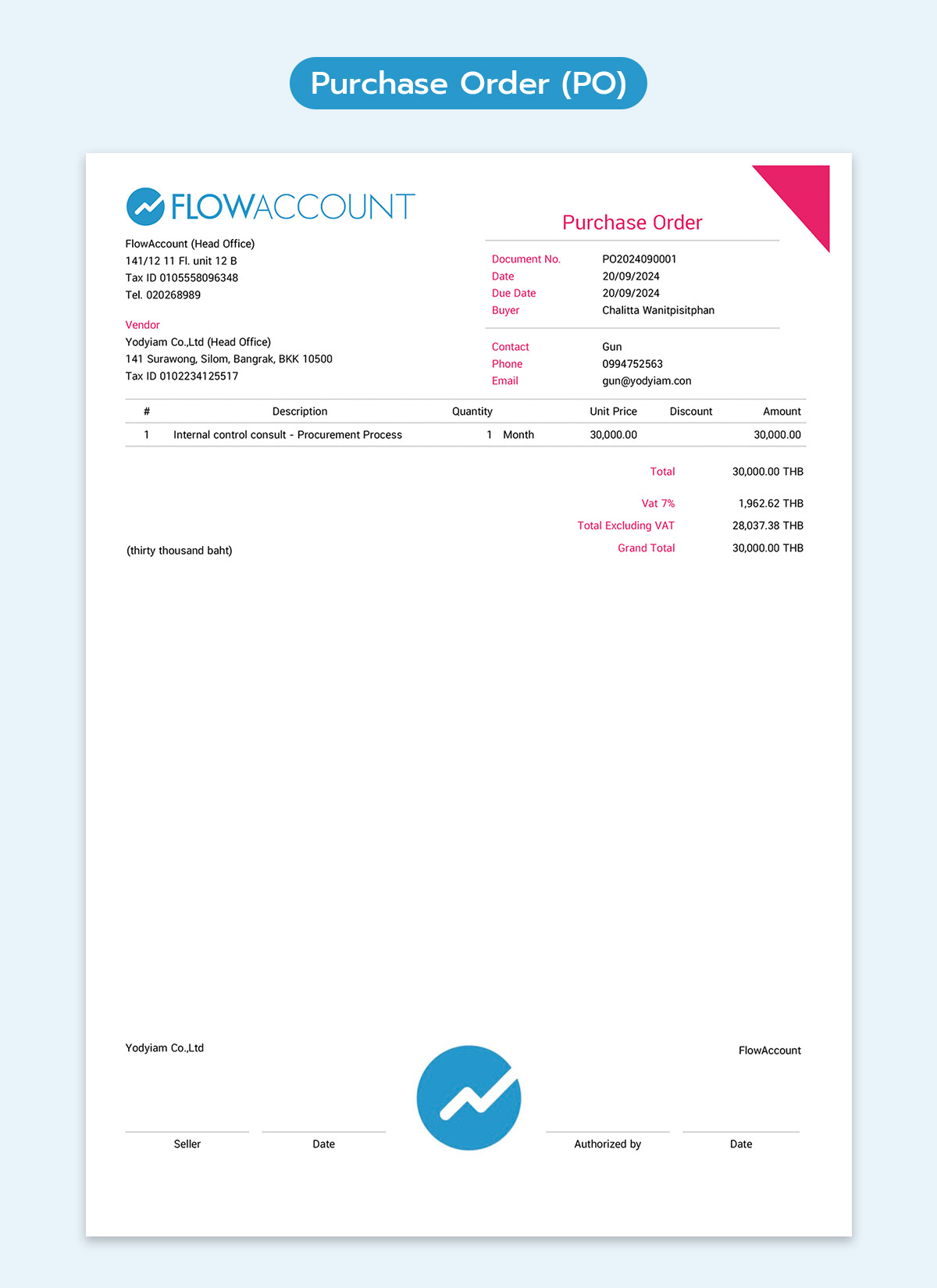

Key Information to Include in a Purchase Order are :

- Name, address, and tax ID of the purchasing company

- Name, address, and tax ID of the selling company

- Purchase order details: number, date, due date, buyer’s name

- Details of the goods or services being ordered

- Quantity of goods or services

- Discount requested from the supplier (as agreed)

- Related VAT

- Preparer and approver

With a clear understanding of what a purchase order is and when it should be used, some might still wonder about its proper use within the process. Where exactly should a purchase order come into play in the procurement cycle to ensure optimal control?

The Difference Between a Purchase Requisition and a Purchase Order

Many people might still be confused about the difference between these two documents, but it’s simple!

The purchase requisition (PR) is used internally within the company to maintain good internal control systems.

When a department in the company needs to purchase any item, they fill out a purchase requisition and specify the item’s type, price, and purpose of use. The purchase requisition needs to be approved by an authorized personnel before proceeding with the purchase to ensure that the item is truly beneficial and necessary for the company.

In most established companies, purchases are only made with approved suppliers to prevent employees from colluding with external suppliers to inflate prices for personal benefit or other frauds.

The purchase order, on the other hand, is an external document sent to suppliers, typically created and approved by the purchasing department to order equipment, items, or products for the company.

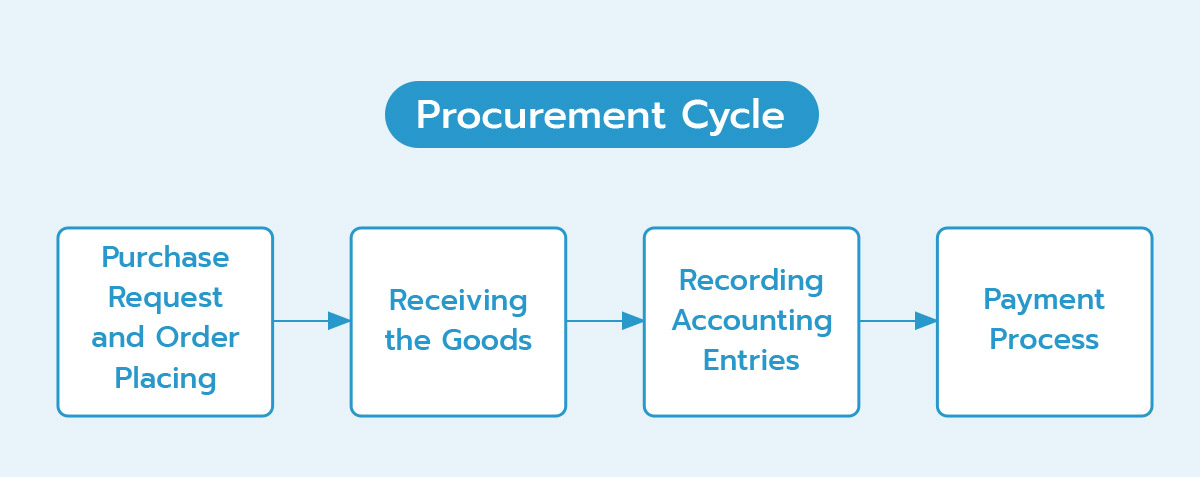

To understand the process better, let’s look at the 4 steps of a procurement cycle which can help ensure effective purchasing operations. This concept can be applied to all purchases whether it’s for inventory or fixed assets.

What are the key steps in an efficient purchasing process?

Here’s an example, focusing primarily on inventory purchases:

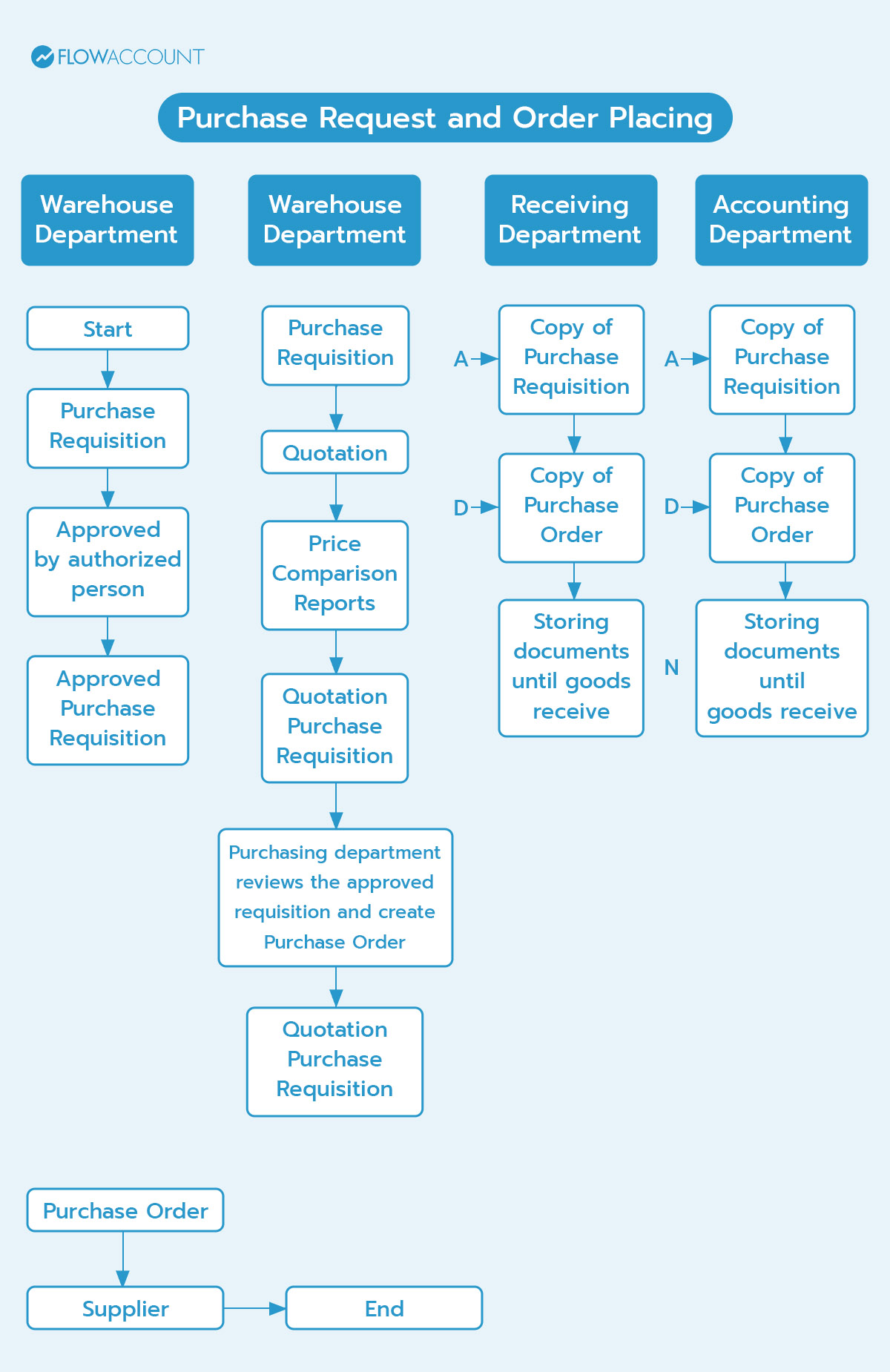

Step 1: Purchase Request and Order Placing

The purchasing cycle starts when different departments, such as the warehouse or the production department, assess when supplies need replenishing. Then, a purchase request will be made.

After the need is identified, the requesting department creates a purchase requisition, which must be approved by authorized personnel. The requisition is then forwarded to relevant departments such as purchasing, accounting, receiving, and kept as a record by the requesting department.

Once the purchasing department receives the requisition, they begin sourcing suppliers to compare prices and quality.

Once a supplier is selected, the purchasing department reviews the approved requisition and creates a “Purchase Order (PO)” to place order with the supplier.

Step 2: Receiving the Goods

When the supplier delivers the goods according to the purchase order (PO), the receiving team inspects the items, ensuring the quantity and type match the details on the goods receipt/ tax invoice, or delivery note issued by the supplier.

- If there are discrepancies, the company can reject the goods and return them to the supplier.

- If everything is correct, the goods will be signed off and stored in the warehouse. The receiving department will then forward the goods receipt and tax invoice to accounting, and send a copy of the receipt to purchasing, keeping another copy as a record at the receiving department.

Step 3: Recording Accounting Entries

Once the accounting department receives the relevant documents, they check the details on the goods receipt, tax invoice/ delivery note against the purchase requisition and purchase order (PO) to ensure accuracy before recording the transaction in the purchase journal.

Step 4: Payment Process

When the payment due date arrives, the supplier sends the invoice to the accounting department to review details of the invoice and approve the payment voucher. Then, the documents are forwarded to the finance department for payment.

The finance department then prepares the cheque for payment to suppliers which is needed to be approved by the authorized signatory.

Once the supplier collects the cheque at the finance department, they sign on a cheque register and provide receipts as evidence of payment. The finance department then stamps the documents with a ‘Paid’ designation to prevent duplicate payments before returning them to accounting for record-keeping.

By following this procurement cycle, businesses can achieve efficient purchasing and minimize any potential inefficiencies or fraud. For those who have never created a Purchase Order (PO), we invite you to try the FlowAccount online accounting program with a 30-day free trial, which includes all features!

About Author

Certified Public Accountant (CPA) Thailand with experience as an external auditor for listed companies who aspires to make accounting easy and accessible for everyone.

Apply to be a writer for FlowAccount here.