What Is Thailand Corporate Income Tax?

Thailand Corporate Income Tax (CIT) is a tax imposed on the net profits earned by companies and certain business entities operating in Thailand. In simple terms, businesses are taxed on the profit remaining after deducting allowable expenses from their revenue, rather than on their total sales or income.

Corporate Income Tax is one of the most important taxes that businesses in Thailand must comply with. Whether you are a local entrepreneur or a foreign investor, understanding how CIT works is essential for managing tax obligations and avoiding potential penalties.

In general, the following entities may be subject to Corporate Income Tax in Thailand:

- Thai Companies and Partnerships

- Foreign Companies

- Carry on business in Thailand, including through employees, agents, or other representatives;

- Carry on business both within and outside Thailand;

- Operate international transportation businesses involving Thailand;

- Derive certain types of Thai-source income, such as service fees, royalties, interest, dividends, or rental income, even without carrying on business in Thailand; or

- Remit profits, or other amounts deemed to be profits, from Thailand to overseas recipients in circumstances prescribed under the Thai Revenue Code.

- Foreign government organizations

- Joint ventures

- Foundations and associations

Who Must Pay Corporate Income Tax in Thailand?

Whether a business is required to pay Corporate Income Tax (CIT) in Thailand depends largely on its legal structure and tax residency status.

Thai tax rules generally distinguish between resident companies and non-resident companies, and the tax treatment may differ depending on how the business operates and where its income is generated.

Resident Companies

A resident company is generally a company incorporated under Thai law. Resident companies are subject to Thai Corporate Income Tax on their worldwide net profits — that is, income derived from business activities both inside and outside Thailand, subject to the provisions of the Thai Revenue Code and any applicable Double Tax Agreements (DTAs).

Examples include:

- Thai Companies and Partnerships

- Thai subsidiaries of foreign groups

Non-Resident Companies

A non-resident company is a foreign company that is not incorporated under Thai law. Unlike resident companies, which are taxed on their worldwide income, non-resident companies are generally taxed only on income derived from Thailand.

Examples include:

- Foreign companies operating through a branch office

- Overseas companies providing services in Thailand

- Foreign businesses receiving certain Thai-source income

Depending on the nature of the income, a non-resident company may be subject to Corporate Income Tax, withholding tax, or both. Tax relief may also be available under an applicable Double Tax Agreement (DTA).

Thailand Corporate Income Tax Rates

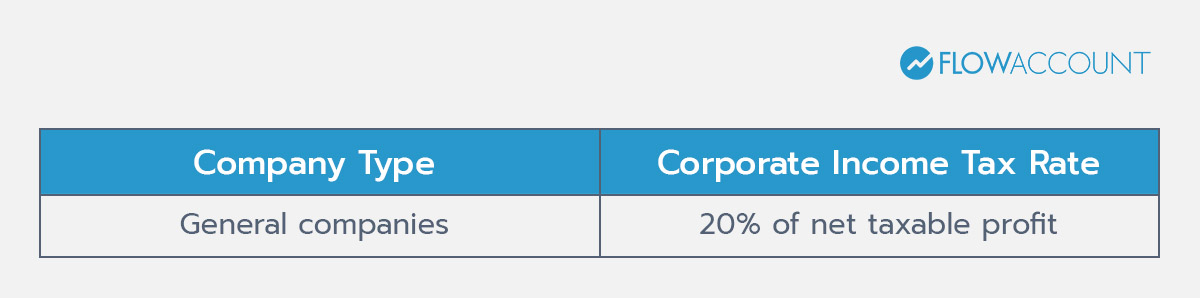

Thailand applies a standard Corporate Income Tax (CIT) rate of 20% on a company's net taxable profit. However, qualifying small and medium-sized enterprises (SMEs) may be eligible for reduced tax rates under Thailand's SME tax regime.

Standard Corporate Income Tax Rate

Most companies operating in Thailand are subject to the following corporate income tax rate:

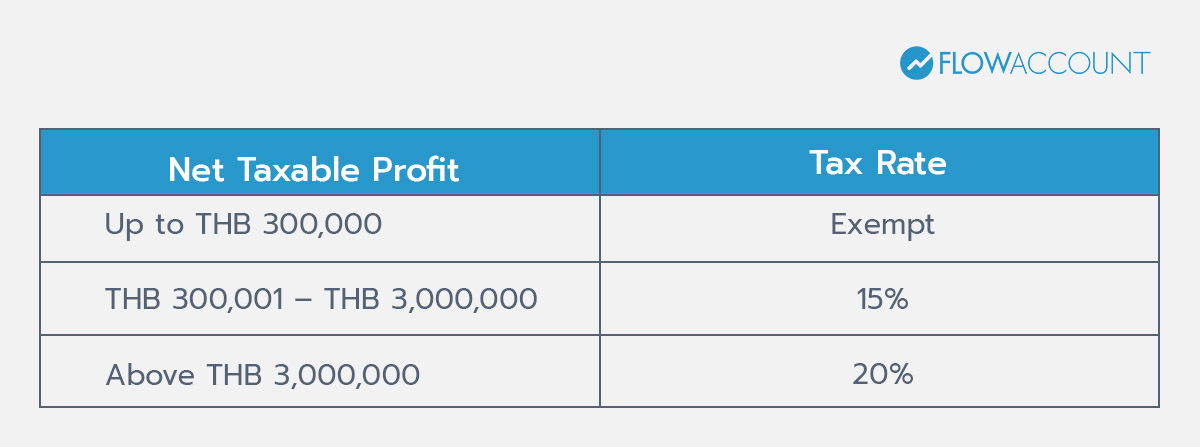

SME Corporate Income Tax Rates

To support smaller businesses, Thailand provides progressive tax rates for qualifying SMEs.

To be eligible, a company must generally meet both of the following conditions:

- Paid-up capital not exceeding THB 5 million at the end of the accounting period

- Annual revenue not exceeding THB 30 million

Tax Incentives and Exemptions

In addition to SME tax benefits, certain businesses may qualify for special tax incentives offered by the Thai government.

For example, companies promoted by the Thailand Board of Investment (BOI) may receive Corporate Income Tax exemptions or Corporate Income Tax reductions for a specified period, depending on the industry and investment activity.

Businesses may also benefit from:

- Double Tax Agreements (DTAs)

- Industry-specific tax incentives

- Special investment promotion schemes

How to Calculate Corporate Income Tax

Corporate Income Tax (CIT) in Thailand is calculated based on a company's net taxable profit, not its total revenue. In other words, businesses pay tax on the profit remaining after deducting allowable expenses and making any required tax adjustments.

The basic calculation can be broken down into four simple steps.

Step 1: Calculate Total Revenue

Start by determining the company's total income for the accounting period. This may include:

- Sales revenue

- Service income

- Rental income

- Interest income

- Other business-related earnings

Step 2: Deduct Allowable Business Expenses

Businesses can generally deduct expenses that are incurred wholly and exclusively for business purposes.

Examples of deductible expenses include:

- Employee salaries and benefits

- Office rent and utilities

- Marketing and advertising expenses

- Professional and consulting fees

- Business travel expenses

- Depreciation of business assets

- Interest on business loans

Maintaining proper supporting documents is essential, as expenses without adequate documentation may not be accepted for tax purposes.

Step 3: Add Back Non-Deductible Expenses

Certain expenses recorded in the accounting records may not be deductible under Thai tax law and must be added back when calculating taxable profit.

Common examples include:

- Personal expenses of shareholders or directors

- Tax penalties and surcharges

- Expenses unrelated to business operations

- Unsupported expenses without valid documentation

As a result, the profit reported in a company's financial statements may not be the same as the profit used to calculate Corporate Income Tax.

Step 4: Calculate Taxable Profit and Apply the Tax Rate

After deducting allowable expenses and adjusting for non-deductible items, the remaining amount is the company's taxable profit.

The Corporate Income Tax payable is then calculated by applying the applicable tax rate — typically 20% for general companies.

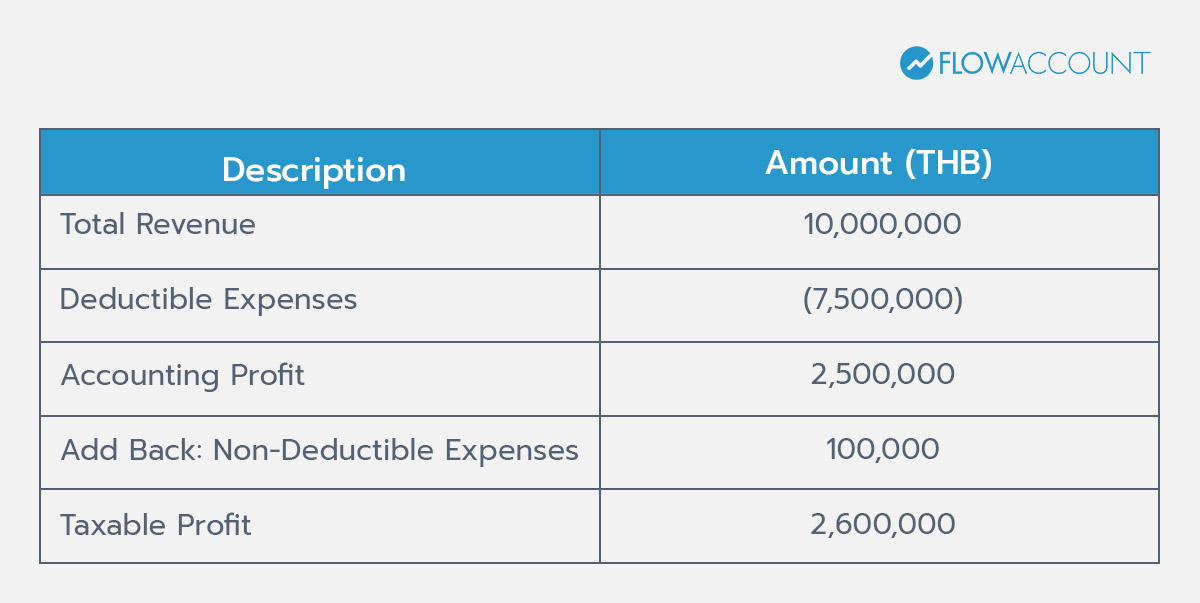

Example of Corporate Income Tax Calculation

Corporate Income Tax Payable:

THB 2,600,000 × 20% = THB 520,000

Why Taxable Profit May Differ from Accounting Profit

The profit reported in a company's financial statements may differ from its taxable profit. This is because tax calculations follow the Thai Revenue Code, which may require certain accounting items to be adjusted before calculating Corporate Income Tax.

Corporate Tax Filing Deadlines in Thailand

Companies operating in Thailand are required to file Corporate Income Tax returns on both a half-year and an annual basis.

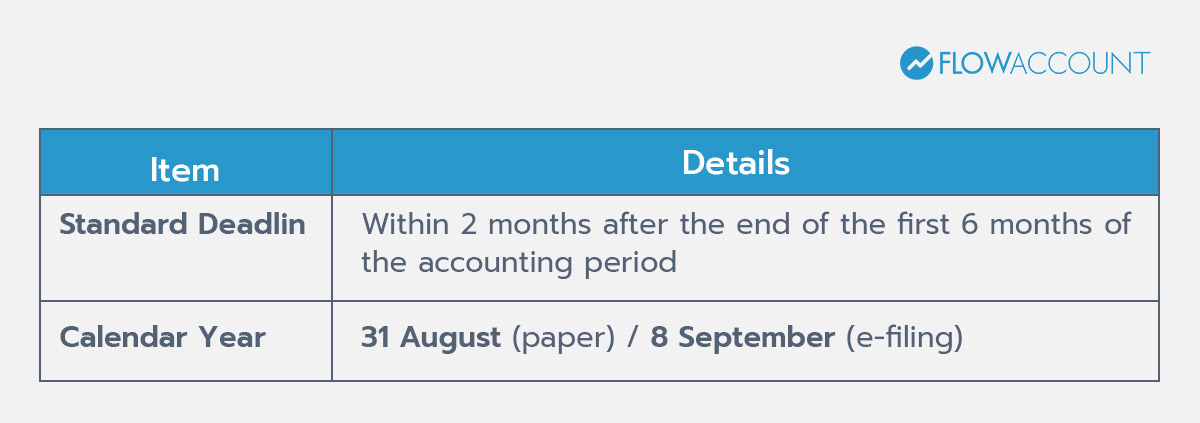

PND 51 (Half-Year Corporate Income Tax Return)

PND 51 is a mid-year tax return based on the company's estimated annual net profit.

For companies using a calendar year (1 January – 31 December), the filing deadline is typically 31 August.

"PND 51 Underestimation Surcharge:If the estimated net profit declared in PND 51 is lower than the actual annual profit by more than 25% without reasonable cause, a 20% surcharge applies to the tax shortfall. Accurate mid-year estimation is therefore important."

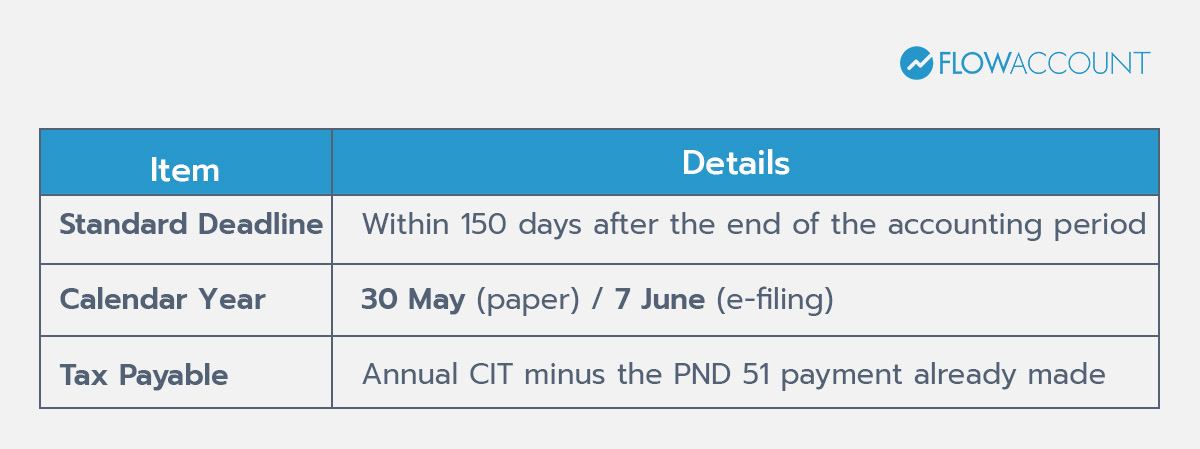

PND 50 (Annual Corporate Income Tax Return)

PND 50 is the annual Corporate Income Tax return based on the company's actual taxable profit for the year.

For companies with a calendar year-end of 31 December, the filing deadline is typically 30 May of the following year.

Online Tax Filing

Businesses can submit both PND 50 and PND 51 electronically through the Revenue Department's e-Filing system, making the filing process more convenient and efficient.

Documents Required for Tax Filing

Before filing Corporate Income Tax returns, businesses should prepare the following documents:

- Audited financial statements

- Profit and loss statement

- Balance sheet

- General ledger and accounting records

- Tax invoices and receipts

- Withholding tax certificates

- Fixed asset register

- Supporting documents for deductible expenses

- Previous tax filings (if applicable)

Maintaining complete and organized records helps reduce filing errors and supports tax audits if required.

Related Taxes Businesses Should Know

In addition to Corporate Income Tax (CIT), businesses operating in Thailand may also be subject to other taxes, particularly Value Added Tax (VAT) and Withholding Tax (WHT).

Value Added Tax (VAT)

VAT is an indirect tax charged on the sale of goods and services in Thailand. Businesses that meet the VAT registration requirements must collect VAT from customers and remit it to the Revenue Department.

The standard VAT rate in Thailand is currently 7%.

Withholding Tax (WHT)

Withholding Tax is a tax deducted at source when certain types of payments are made, such as:

- Service fees

- Rental payments

- Advertising expenses

- Transportation expenses

- Professional and consulting fees

- Dividends

- Interest

Withholding Tax is paid to the Revenue Department on behalf of the recipient and can generally be claimed as a tax credit when calculating Corporate Income Tax.

Tax Incentives and Exemptions

Thailand offers a range of tax incentives designed to encourage investment, business growth, and economic development. Depending on the nature of the business, companies may qualify for tax benefits that can help reduce their overall tax burden.

BOI Incentives

The Thailand Board of Investment (BOI) provides tax incentives to businesses operating in promoted industries, such as technology, manufacturing, renewable energy, and digital services.

Depending on the approved project, BOI-promoted companies may be eligible for:

- Corporate income tax exemptions

- Corporate income tax reductions

- Import duty exemptions on machinery and raw materials

- Other investment-related benefits

SME Tax Benefits

Qualified small and medium-sized enterprises (SMEs) may benefit from reduced Corporate Income Tax rates. These preferential rates are intended to support smaller businesses and encourage entrepreneurship in Thailand.

Double Tax Agreements (DTAs)

Thailand has entered into Double Tax Agreements (DTAs) with many countries to help prevent the same income from being taxed twice.

Depending on the applicable treaty, businesses may benefit from:

- Reduced withholding tax rates

- Relief from double taxation

- Greater certainty regarding cross-border tax obligations

Since eligibility and benefits vary, businesses should review the relevant requirements or seek professional advice before claiming any tax incentives or exemptions.

Penalties for Late Tax Filing

Failing to file Corporate Income Tax returns on time can result in additional costs and compliance risks for businesses operating in Thailand.

Depending on the circumstances, late filing may lead to:

- Financial penalties for late submission

- Surcharges and interest on unpaid taxes

- Additional tax assessments by the Revenue Department

- Increased risk of tax audits and compliance reviews

These consequences can increase a company's overall tax costs and create unnecessary administrative burdens.

How to Avoid Tax Filing Penalties

Businesses can reduce the risk of late filing and tax errors by:

- Maintaining accurate accounting records throughout the year

- Preparing monthly financial reports

- Keeping tax invoices, receipts, and supporting documents organized

- Monitoring tax filing deadlines regularly

- Reviewing tax calculations before submission

- Seeking professional accounting or tax advice when necessary

FlowAccount Makes Corporate Income Tax Management Easier

Calculating corporate income tax requires accurate records of income, expenses, and supporting accounting documents. When financial information is disorganized, businesses may face calculation errors, delayed tax filings, or spend unnecessary time gathering documents at the end of the accounting period. This is especially true for companies with foreign shareholders or management teams who may not yet be familiar with Thailand's accounting and tax requirements.

FlowAccount simplifies accounting and tax management by allowing businesses to record income and expenses, issue sales documents, and keep all financial data organized in one system. With comprehensive accounting reports, business owners and accountants can easily monitor financial performance and use accurate data to support corporate income tax calculations. Whether you are a Thai entrepreneur or a foreign business owner operating in Thailand, FlowAccount helps you manage your financial records efficiently and reduce errors caused by scattered documents or multiple spreadsheets.

Thailand Corporate Income Tax is an important responsibility for every business operating in Thailand. Keeping accurate accounting records and filing taxes on time helps businesses stay compliant, reduce tax risks, and support sustainable growth.

(FAQ) Thailand Corporate Income Tax 2026

1. What is the corporate tax rate in Thailand?

Answer: The standard Corporate Income Tax (CIT) rate in Thailand is 20% of net taxable profit. Qualifying SMEs may be eligible for reduced tax rates.

2. When do companies file PND 50?

Answer: Companies must file PND 50 within 150 days after the end of their accounting period. For companies with a 31 December year-end, the filing deadline is typically 30 May of the following year.

3. Do foreign companies pay tax in Thailand?

Answer: Yes. Foreign companies earning income from Thailand or carrying on business activities in Thailand may be subject to Corporate Income Tax, withholding tax, or both, depending on the nature of the income.

4. What expenses are tax deductible?

Answer: Common deductible expenses include salaries, rent, utilities, advertising costs, professional fees, and other expenses incurred wholly and exclusively for business purposes, provided adequate supporting documents are maintained.

5. What happens if tax is filed late?

Answer: Late filing may result in penalties, surcharges, and interest on unpaid taxes. It may also increase the risk of a tax audit by the Revenue Department.